So much for John Key's 'rockstar economy.'

Mainstream news - Ambrose Evans-Pritchard of the Telegraph, no less.

Mind you he predicted the imminent collapse of Russia's economy last year.

HSBC fears world recession with no lifeboats left

The world authorities have run out of ammunition as rates remain stuck at zero. They have no margin for error as economy falters

By Ambrose

Evans-Pritchard

26

May, 2015

The

world economy is disturbingly close to stall speed. The United

Nations has cut its global growth forecast for this year to 2.8pc,

the latest of the multinational bodies to retreat.

We

are not yet in the danger zone but this pace is only slightly above

the 2.5pc rate that used to be regarded as a recession for the

international system as a whole.

It

leaves a thin safety buffer against any economic shock – most

potently if China abandons its crawling dollar peg and resorts to

‘beggar-thy-neighbour’ policies, transmitting a further

deflationary shock across the global economy.

The

longer this soggy patch drags on, the greater the risk that the

six-year old global recovery will sputter out. While expansions do

not die of old age, they do become more vulnerable to all kinds of patholыogies.

A

sweep of historic data by Warwick University found compelling

evidence that economies are more likely to stall as they age, what is

known as “positive duration dependence”. The business cycle

becomes stretched. Inventories build up and companies defer spending,

tipping over at a certain point into a self-feeding downturn.

Stephen

King from HSBC warns that the global authorities have alarmingly few

tools to combat the next crunch, given that interest rates are

already zero across most of the developed world, debts levels are at

or near record highs, and there is little scope for fiscal stimulus.

“The

world economy is sailing across the ocean without any lifeboats to

use in case of emergency,” he said.

In

a grim report – “The World Economy’s Titanic Problem” – he

says the US Federal Reserve has had to cut rates by over 500 basis

points to right the ship in each of the recessions since the early

1970s. “That kind of traditional stimulus is now completely ruled

out. Meanwhile, budget deficits are still uncomfortably large,” he

said.

The

authorities are normally able to replenish their ammunition as

recovery gathers steam. This time they are faced with a chronic

low-growth malaise – partly due to a global ‘savings glut’, and

increasingly to a slow ageing crisis across most of the Northern

hemisphere. The Fed keeps having to defer its first rate rise as

expectations fall short.

Each

of the past four US recoveries has been weaker than the last one. The

average growth rate has fallen from 4.5pc in the early 1980s to

nearer 2pc this time. The US fiscal deficit has dropped to 2.8pc but

is expected to climb again as pension and health care costs bite,

even if the economy does well.

The

US cannot easily launch a fresh New Deal. Public debt was just 38pc

on GDP when Franklin Roosevelt took power in 1933, and there were few

contingent liabilities hanging over future US finances.

“Fiscal

stimulus – a novel idea at the time – may have been

controversial, but the chances of it working to boost economic

activity were quite high given the healthy starting position. Today,

it is much more difficult to make the same argument,” he said.

The

great hope – and most likely outcome – is that the recent

monetary expansion in the US and the eurozone starts to gain traction

later this year. Broad ‘M3′ money data – a one-year advance

indicator – has been growing briskly on both sides of the Atlantic.

But nobody knows for sure whether the normal monetary mechanisms are

working.

JP

Morgan estimates that the US economy contracted at an rate of 1.1pc

in the first quarter, far worse than originally supposed.

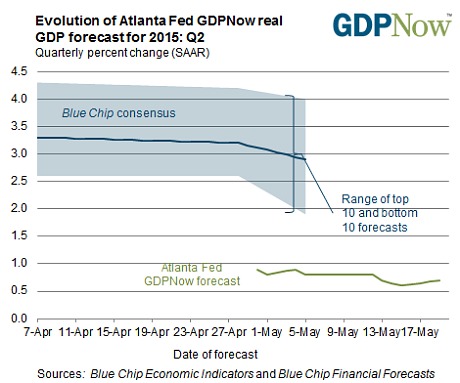

The

instant tracking indicator of the Atlanta Fed – GDPnow – shows

little sign that America is shaking off its mystery virus. Growth was

just 0.7pc (annualised) in mid-May. It is becoming harder to argue

the relapse is a winter blip or caused by temporary gridlock at

California ports.

Over

100,000 lay-offs across the oil and gas belt seem to have taken their

toll. The Fed thought the windfall gain of cheaper energy for

everybody else would weigh more in the balance, but this time

Americans have chosen to salt away the money.

Net

saving jumped by $125bn to $728bn in the first quarter. There was no

pick-up in April. Retail sales were flat.

It

is now more likely than not that US economy has dropped through the

Fed’s stall-speed threshold of two consecutive quarters below 2pc

growth. Exactly how far below is unclear. The Fed uses its own growth

measure – gross domestic income (GDI) – and this data has not yet

been published.

The

stall speed concept is soft science but not to be ignored. “Output

tends to transition to a slow-growth phase at the end of expansions,”

said a Fed research paper.

Much

now depends on China, where the economy is starting to look

“Japanese”. Dario Perkins from Lombard Street Research says the

Chinese economy is in a much deeper downturn than admitted so far by

the authorities. It probably contracted outright in the first

quarter.

Electricity

use has turned negative. Rail freight has been falling at near

double-digit rates. What began as a deliberate move by Beijing to

choke off a credit bubble has taken on a life of its own, evolving

into a primordial balance-sheet purge.

It

was inevitable that China’s investment bubble would lead to vast

inventory of unsold property. The country produced more cement

between 2011 and 2013 than the US in the 20th Century –

Mr

Perkins said China is now in a “classic debt deflation spiral” as

excess capacity holds down prices. Factory gate inflation is now

minus 4.6pc. This in turn is tightening the noose further by pushing

up real borrowing costs.

The

Chinese authorities have so far resisted the temptation to flood the

system with fresh stimulus, fearing that this would store up even

greater trouble.

They

have taken steps to offset a clampdown on local government spending

and avert a “fiscal cliff” that might otherwise have occurred.

They have loosened policy for banks just enough to offset the

contractionary effects of capital flight. But they have not yet come

to the rescue.

This

matters enormously. Andrew Roberts from RBS says China accounted for

85pc of all global growth in 2012, 54pc in 2013, and 30pc in 2014.

This is likely to fall to 24pc this year. “If there is only one

statistic that you need to know in the world right now, this is it,”

he said.

The

effects are being felt across Asia. Japan keeps disappointing. Its

exports to China have fallen 15pc over the last year. Korea is

flirting with recession.

Russia,

Brazil, Argentina, and Venezuela are all contracting sharply,

casualties of the China-driven commodity bust. The UN says the growth

rate for the emerging market nexus (ex-China) has dropped to 2.3pc

from an average of 6.5pc in the glory years of 2004-2007.

Europe

is doing better but it is hardly a boom. The eurozone is contributing

little to global demand. The region has displaced China and to become

the world’s “saver of last resort” – or its biggest black

hole in the view of critics – exploiting the weaker euro to rack up

a current account surplus of $358bn.

It

is far from clear whether Europe can act as an engine of world

recovery. The composite purchasing managers index (PMI) for services

and manufacturing slipped in May, and new orders fell. Oxford

Economics thinks the “sugar rush” from quantitative easing may be

wearing off.

HSBC’s

Mr King says the global authorities face awful choices if the world

economy hits the reefs in its current condition. The last resort may

have to be “helicopter money”, a radically different form of QE

that injects money directly into the veins of economy by funding

government spending.

It

is a Rubicon that no central bank wishes to cross, though the Bank of

Japan is already in up to the knees.

The

imperative is to avoid any premature tightening or policy error that

could crystallize the danger. As Mr King puts it acidly. “Many –

including the owner of the Titanic – thought it was unsinkable: its

designer, however, was quick to point out that ‘She is made of

iron, sir, I assure you she can’.”

No comments:

Post a Comment

Note: only a member of this blog may post a comment.